Emergency Services 24/7

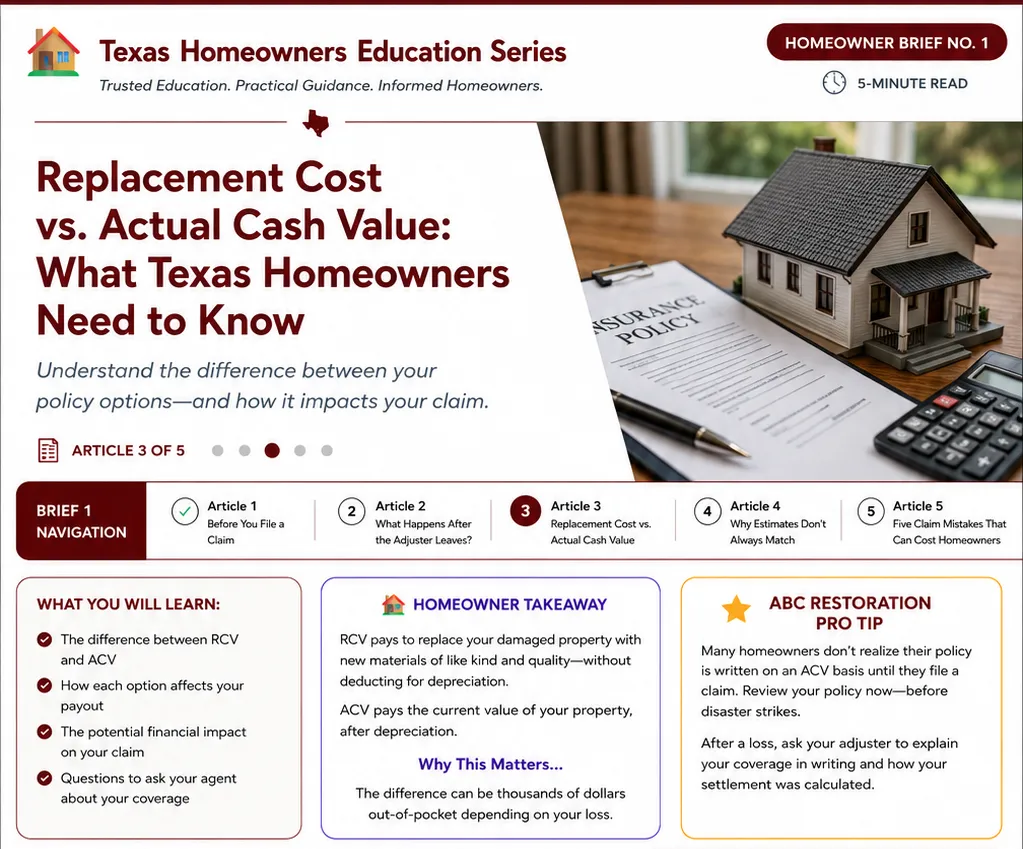

What Is Replacement Cost Value (RCV)?

Replacement Cost Value represents the estimated cost to repair or replace damaged property with similar materials and quality without subtracting depreciation. It covers what it actually cost to rebuild or replace your home or belongings in TODAYS economy at TODAYS condition.

In simple terms:

RCV = The cost to replace something today.

For example:

A hailstorm damages your roof.

The estimated cost to replace the roof is:

$18,000

If your policy includes replacement cost coverage, the claim may be based on the current cost to replace that roof.

What Is Actual Cash Value (ACV)?

Actual Cash Value takes depreciation into account.

Depreciation reflects that materials and property generally lose value over time because of age, wear, and condition. Which means the payout is based on the current value of the property at time of loss-not what it would cost to replace it. Older roofs, flooring, appliances and other items may be valued at a fraction of their replacement cost.

In simple terms:

ACV = Replacement Cost minus depreciation.

Example:

A roof needs replacement.

Current replacement cost:

$18,000

Depreciation based on roof age:

$6,000

Actual Cash Value:

$12,000

The insurance payment may begin with the ACV amount depending on the terms of the policy.

What Is Depreciation?

Depreciation is one of the biggest reasons homeowners become confused during a claim.

Insurance companies may consider factors such as:

Age of the damaged item

Expected lifespan

Condition before the damage occurred

Type of material

For example:

A brand-new roof and a 15-year-old roof may require the same repair today, but they may not have the same value under an insurance policy.

Recoverable Depreciation: What Does That Mean?

Some policies allow homeowners to recover depreciation after repairs are completed.

This may work like this:

Insurance calculates the repair cost.

The initial payment may be based on Actual Cash Value.

After approved repairs are completed, additional funds may be available.

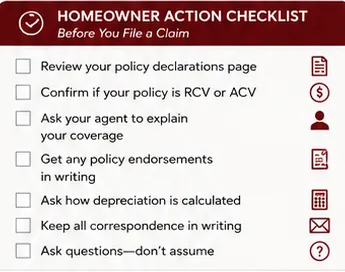

Because every policy is different, homeowners should ask their insurance company how depreciation applies to their specific claim.

Why Roof Age Matters in Texas

Texas homeowners should pay close attention to how their policy handles roof damage.

Severe weather, including hail and wind events, can create significant roof damage. However, the age and condition of the roof may impact how the claim is calculated.

Homeowners should understand:

Their roof coverage

How depreciation is applied

Whether replacement cost coverage applies

Any policy limitations

Why This Matters?

If your policy is written on an ACV basis, you could be left to pay-out-of-pocket for thousands of dollars to fully retore your home. Many homeowners don't realize this until it's too late.

Frequently Asked Questions

Can I change my coverage?

Yes! You can switch from ACV to RCV (or add RCV for specific items) at renewal.

Does RCV cost more?

Yes, but the additional premium is often small compared to the out of pocket savings.

Will my claim automatically/always be paid as RSV?

Some policies pay ACV upfront and the RSV after repairs are complete. Ask your agent how your policy works BEFORE signing.

Should I upgrade my policy?

If you have older items or live in a growing area like Texas, an RSV policy is usually the better protection.

Did You Know?

Many homeowners assume the first insurance payment is the final amount they will receive.

Depending on the policy and claim circumstances, additional funds may become available after repairs are completed and required documentation is provided.

Browse All Briefs

RESOURCE LIBRARY

Helpful guides, tools and additional resources for all stages.

~ Downloadable Action Guides ~

Homebuyer Repair Planning Guide

Insurance Claim

Prep Guide

Home Project Budget Guide

Contractor Estimate Comparison Guide

Texas Homeowner Roofing Guide

Storm Damage Inspection Guide

Emergency Contact Guide

Annual Home Maintenance Guide

Finance Comparison Guide

~ Explore Additional Volumes & Resources ~

~ Explore Learning Paths~

Trusted Education

Practical Guidance

Informed Decisions

FOLLOW US

COMPANY

Resource Center

Contact Us

Copyright . . All Rights Reserved.