Emergency Services 24/7

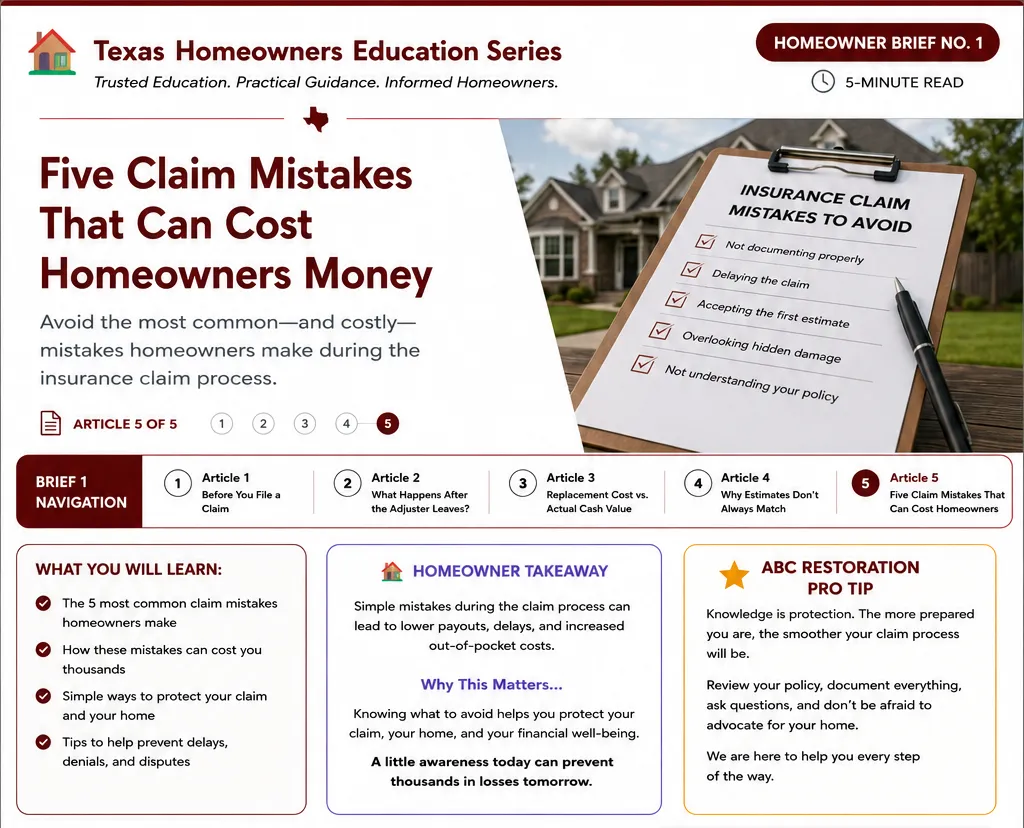

The Five Most Common Claim Mistakes Homeowners Make

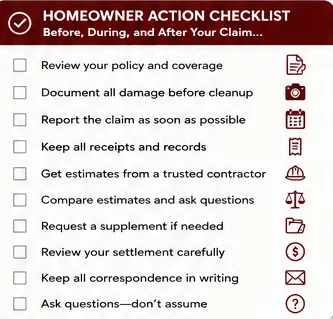

Filing a homeowners insurance claim can feel overwhelming, especially when you're dealing with unexpected property damage. Between documenting the loss, speaking with your insurance company, arranging inspections, and protecting your home from further damage, it's easy to overlook important details.

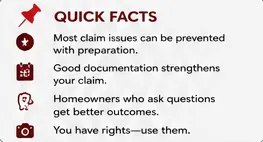

Fortunately, many of the most common claim problems are preventable. By understanding where homeowners often run into trouble, you can help keep your claim organized, reduce unnecessary delays, and improve communication throughout the restoration process.

Here are five common mistakes—and how to avoid them.

1. Not Documenting the Damage Thoroughly

One of the biggest mistakes homeowners make is failing to fully document the damage before beginning cleanup or temporary repairs. Photos and videos taken immediately after a loss provide valuable evidence of the property's condition and can help support your insurance claim if questions arise later.

Take clear photographs from multiple angles, capture both close-up and wide views, and keep copies of any receipts for emergency repairs or protective measures.

Homeowner Tip: Document first whenever it is safe to do so, then begin temporary mitigation to help prevent additional damage.

2. Waiting Too Long to Report the Loss

While every insurance policy is different, unnecessary delays in reporting property damage can complicate the claims process. Waiting too long may make it more difficult to determine the cause of damage or demonstrate when the loss occurred.

If you believe damage may exceed your deductible or require professional repairs, contact your insurance company promptly after documenting the property and taking reasonable steps to prevent further damage.

3. Accepting the First Estimate Without Reviewing It

Many homeowners assume the initial insurance estimate represents the complete scope of repairs. In reality, an estimate is based on the information available during the inspection, and additional damage may not always be visible at first.

Carefully review the estimate and compare it with your contractor's repair proposal. If legitimate differences exist because of hidden damage, building code requirements, or omitted items, additional documentation may be submitted for review through the supplement process.

Understanding what is—and is not—included helps homeowners make more informed decisions before repairs begin.

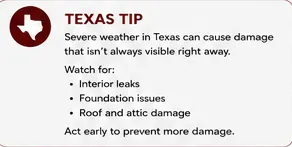

4. Overlooking Hidden Damage

Not all storm or water damage is immediately visible. Missing shingles may be obvious, but moisture behind walls, damaged roof decking, compromised flashing, or structural issues often require a closer inspection.

Professional restoration contractors frequently discover additional damage after work begins, which is why repairs sometimes require updated insurance documentation.

Ignoring hidden damage can allow small problems to become much larger and more expensive over time.

5. Not Understanding Your Insurance Policy

Many claim frustrations occur simply because homeowners are unfamiliar with their policy before a loss happens. Understanding your deductible, coverage limits, depreciation, exclusions, and whether your policy pays Replacement Cost Value (RCV) or Actual Cash Value (ACV) can help set realistic expectations throughout the claims process.

Reviewing your policy before an emergency—and asking questions when something is unclear—can help you make more confident decisions when you need them most.

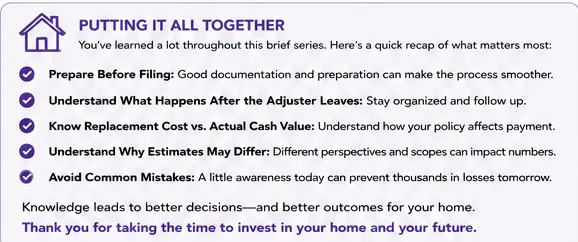

Homeowner Takeaway

Insurance claims don't have to be confusing. Most delays and frustrations occur because homeowners are forced to make important decisions during stressful situations. A little preparation, good documentation, and clear communication with your insurance company and restoration contractor can make the process much smoother.

The goal isn't simply to file a claim—it's to properly restore your home while protecting your investment.

Frequently Asked Questions

Will filing a claim increase my rate?

It can. It depends on your insurance company, your state, and the details of your claim.

Can I choose my own contractor?

Yes! You have the right to choose the contractor you trust!

What if I discover more damage?

You can request a supplement from your insurance company.

How long do I have to file a claim?

It depends on your policy and the type of loss. Check your policy for deadlines.

Did You Know?

Many homeowners are surprised to learn that an insurance claim can continue to change even after the initial estimate is written.

As repairs begin, contractors sometimes discover hidden damage that wasn't visible during the original inspection. When properly documented, these additional findings may be submitted to the insurance company for review through a supplement. This is a normal part of many property restoration projects and helps ensure the repair scope reflects the actual damage—not just what could be seen on day one.

Browse All Briefs

RESOURCE LIBRARY

Helpful guides, tools and additional resources for all stages.

~ Downloadable Action Guides ~

Homebuyer Repair Planning Guide

Insurance Claim

Prep Guide

Home Project Budget Guide

Contractor Estimate Comparison Guide

Texas Homeowner Roofing Guide

Storm Damage Inspection Guide

Emergency Contact Guide

Annual Home Maintenance Guide

Finance Comparison Guide

~ Explore Additional Volumes & Resources ~

~ Explore Learning Paths~

Trusted Education

Practical Guidance

Informed Decisions

FOLLOW US

COMPANY

Resource Center

Contact Us

Copyright . . All Rights Reserved.